AML (Anti-Money Laundering)

Combating Financial Crime: Understanding Anti-Money Laundering (AML)

AML or Anti-Money Laundering refers to a set of procedures, laws, or regulations designed to stop the practice of generating income through illegal activities. 'Money laundering' is the process in which criminals undertake a series of steps that make it look like money made from illegal or unethical activities was earned legitimately and can enter the traditional banking system. Most anti-money laundering programs focus on the source of funds as opposed to anti-terrorism and similar programs which focus on the destination of funds. In modern finance, a typical anti-money laundering program would be run by financial institutions to analyze customer data and detect suspicious transactions.

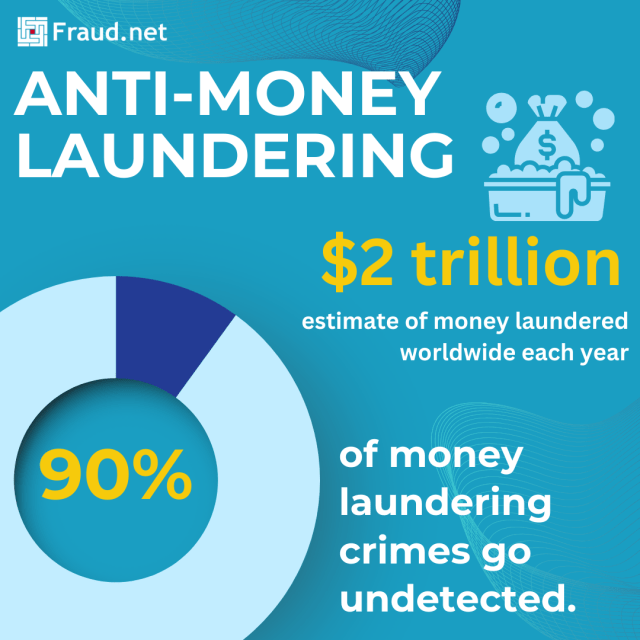

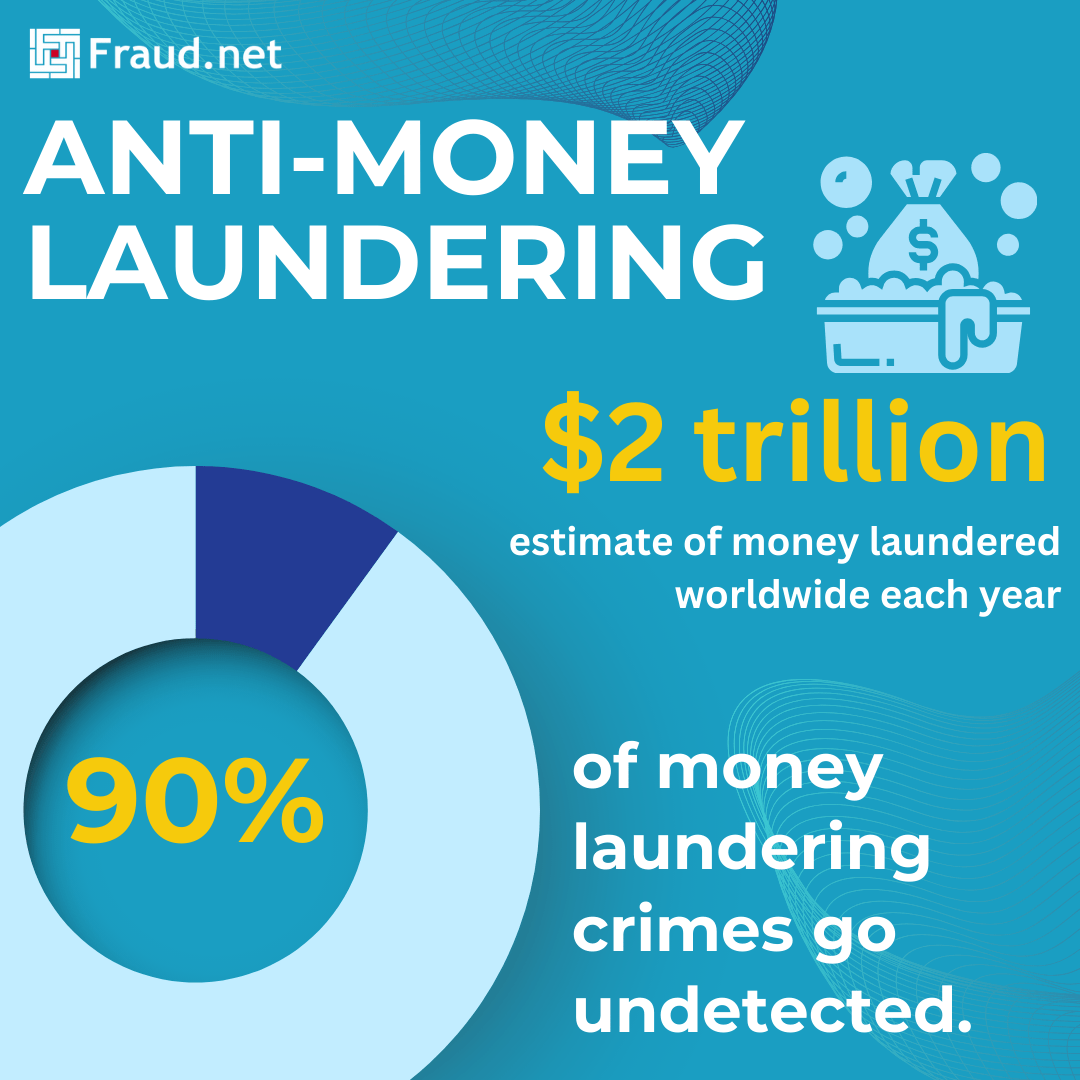

Did you know?

- 300 billion is laundered through the United States each year

- Worldwide, criminals launder between $800 million and $2 trillion each year.

- 90% of money laundering crimes go undetected.

What is AML?

Anti-Money Laundering, commonly known as AML, refers to a set of laws, regulations, and procedures aimed at preventing individuals and organizations from concealing the origins of illegally obtained money. The primary goal of AML is to detect and deter money laundering activities, which typically involve three main stages: placement, layering, and integration. These activities are used to legitimize funds obtained through illegal means, such as drug trafficking, fraud, corruption, or terrorism.

Common Types of Money Laundering:

Money laundering typically consists of three primary stages:

- Placement: Introducing illegal funds into the legitimate financial system.

- Layering: Creating complex layers of transactions to obscure the money's source.

- Integration: Reintroducing laundered funds into the economy, making them appear legitimate.

AML focuses on identifying and preventing these activities by requiring financial institutions to implement safeguards, report suspicious transactions, and maintain comprehensive records.

Six Key AML Solutions

A robust AML program involves a combination of measures that aim to identify, monitor, and report suspicious activities.

The six most popular solutions include:

- Customer Due Diligence (CDD): Verifying the identity of customers and assessing their risk profile.

- Transaction Monitoring: Tracking and analyzing transactions to detect unusual or suspicious behavior.

- Suspicious Activity Reporting: Reporting potential money laundering activities to the appropriate authorities.

- Record-keeping: Maintaining comprehensive records of customer information, transactions, and risk assessments.

- Employee Training: Ensuring that employees are educated and trained to recognize and report suspicious activities.

- Regulatory Compliance: Staying up-to-date with AML laws and regulations to adapt to evolving risks.

Strengthen Your AML Defense with Fraud.net.

Fraud.net is a leading provider of advanced solutions for AML and KYC monitoring. Their platform offers a comprehensive suite of tools to help organizations effectively combat money laundering and other financial crimes and achieve compliance with local regulations.

To learn more about how Fraud.net can tailor a solution to meet your specific AML needs and explore their other capabilities, book a demo and speak with one of our solutions consultants today!