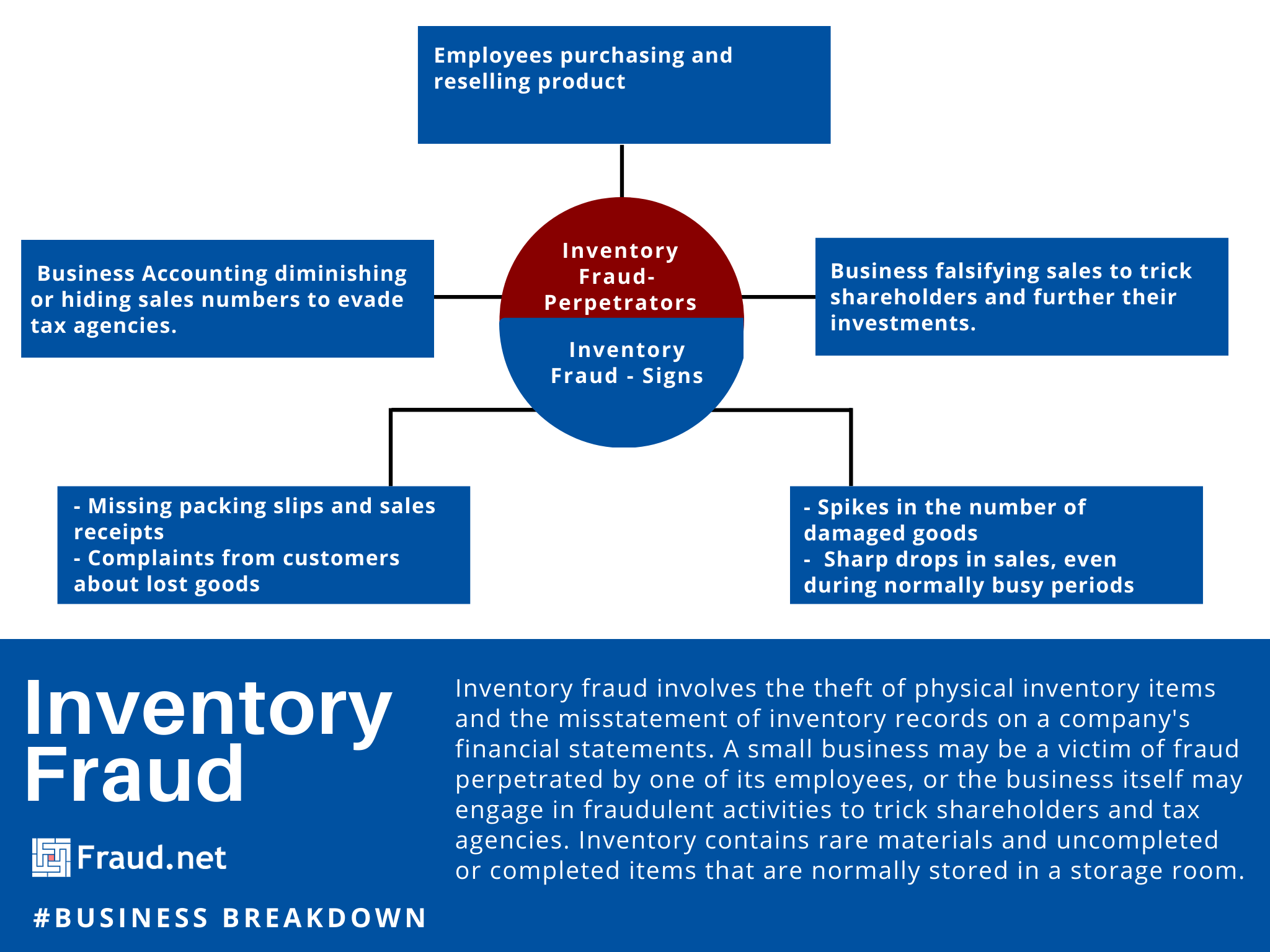

Inventory fraud involves the theft of physical inventory items and the misstatement of inventory records on a company’s financial statements. A small business may be a victim of fraud perpetrated by one of its employees, or the business itself may engage in fraudulent activities to trick shareholders and tax agencies. Inventory contains rare materials and uncompleted or completed items that are normally stored in a storage room.

Inventory is one of the biggest assets on a manufacturer’s balance sheet. It’s also one of the hardest assets to measure and track. Therefore, protecting it becomes essential for direct growth. Timely fraud detection and prevention can save your business essential time and money.

Inventory Fraud: Warning Signs

Telling signs of fraud include missing packing slips and sales receipts, complaints from customers about lost goods, spikes in the number of damaged goods and sharp drops in sales, even during normally busy periods. These events can happen on a digital or physical level. Falsifying orders online, or purchasing orders for resale, is another way company employees might try to benefit.

In a June 2001 article for Journal of Accountancy, Joseph T. Wells, founder and chairman of the Association of Certified Fraud Examiners, wrote about several risk factors for what he called “phantom inventories”. To clarify, The term refers to companies who falsify their information to trick tax agencies or shareholders. Attempts to fool company investors may include bogus purchase orders, fabricated shipping and receiving reports, and inflated inventory counts. Fraudsters might even stack empty packing boxes in the company warehouse to feign inventory.

Protect Your Business

To prevent theft in physical warehouses and in offices, make sure to lock storage areas, install video monitoring and alarm systems. Likewise, consider running background checks on employees and conducting physical audits of your inventory at a random interval. As businesses digitize, it’s important to have a system in place to assess the risk of customers and their purchases. A system like Fraud.net performs real-time assessments, sometimes hundreds of times per second, of payments, identities, and other data to determine risk even before the point of purchase. Online fraud systems identify and halt anomalous and problematic flare-ups as they happen to help you get in front of potential fraud.

You can prevent inventory fraud by building an environment with the right controls. Learn more about Fraud.net’s end-to-end anti-fraud solution and other tools you can leverage to mitigate threats.